Estimated reading time: 4 minutes

President Donald Trump says the US economy is finally his. Now he’ll have to defend it.

Early in his second term, Trump’s team argued it might take a year before he could fully claim ownership of the economy. On Super Bowl Sunday a few weeks ago, he declared: “We’re there now.” Convincing Americans of that — in his State of the Union address and throughout months of midterm campaigning — may prove difficult.

Many voters don’t seem persuaded by Trump’s repeated assertion that the nation is experiencing the “greatest economy” ever. A recent Washington Post-ABC News-Ipsos poll showed majorities disapprove of his handling of the economy, inflation and tariffs.

Presidents often struggle to claim credit for good economic news while distancing themselves from bad developments. Trump faces a mix of both in the latest data. The labor market is holding up, but inflation remains persistent — a potentially decisive issue in November’s midterms, as voters fatigued by years of high prices focus on affordability.

“The actual economy is fairly solid, but voters are probably not going to see it that way,” said Stephanie Roth, chief economist at Wolfe Research. “People feel things are unaffordable, and the administration cannot fix that.”

Some Republicans have voiced frustration that the White House hasn’t articulated a clearer message on cost-of-living pressures. Trump last week shifted tone, telling supporters at a rally in battleground Georgia that he had “won” on affordability.

Here’s what the latest data show about Trump’s economy:

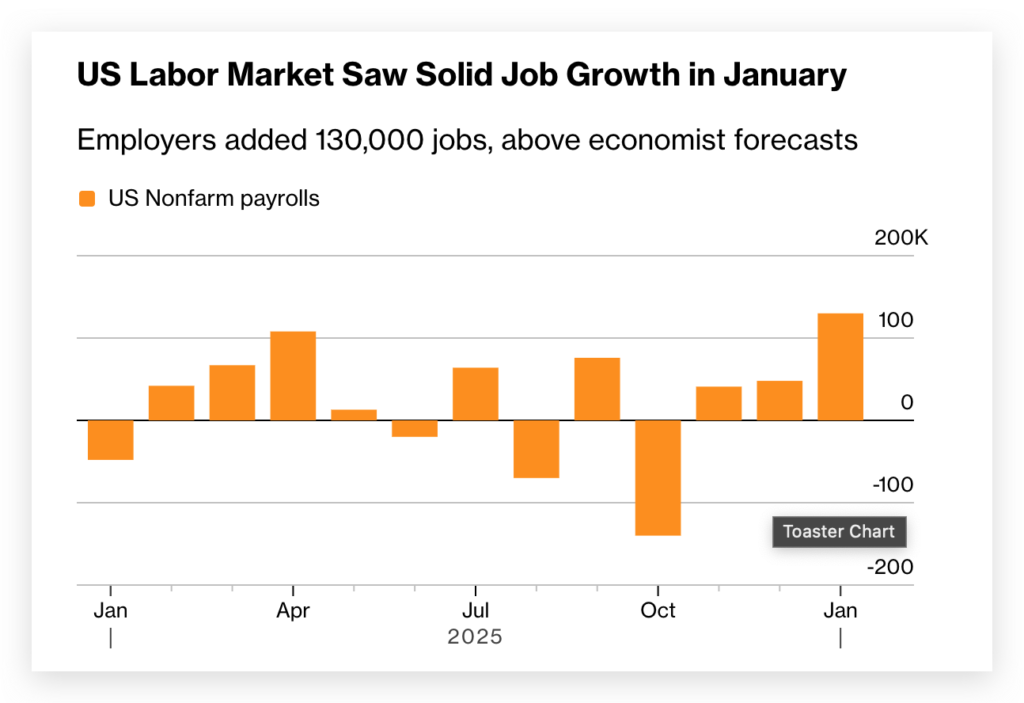

Job Growth, Wages

The labor market has shown signs of stabilizing after slowing last year. Employers added 130,000 jobs in January, compared with an average of just 15,000 per month in 2025, and the unemployment rate dipped to 4.3%.

Wage growth has also outpaced consumer prices, giving workers real income gains. Still, average hourly earnings rose 3.7% from a year earlier in January — a slower pace than before Trump returned to office.

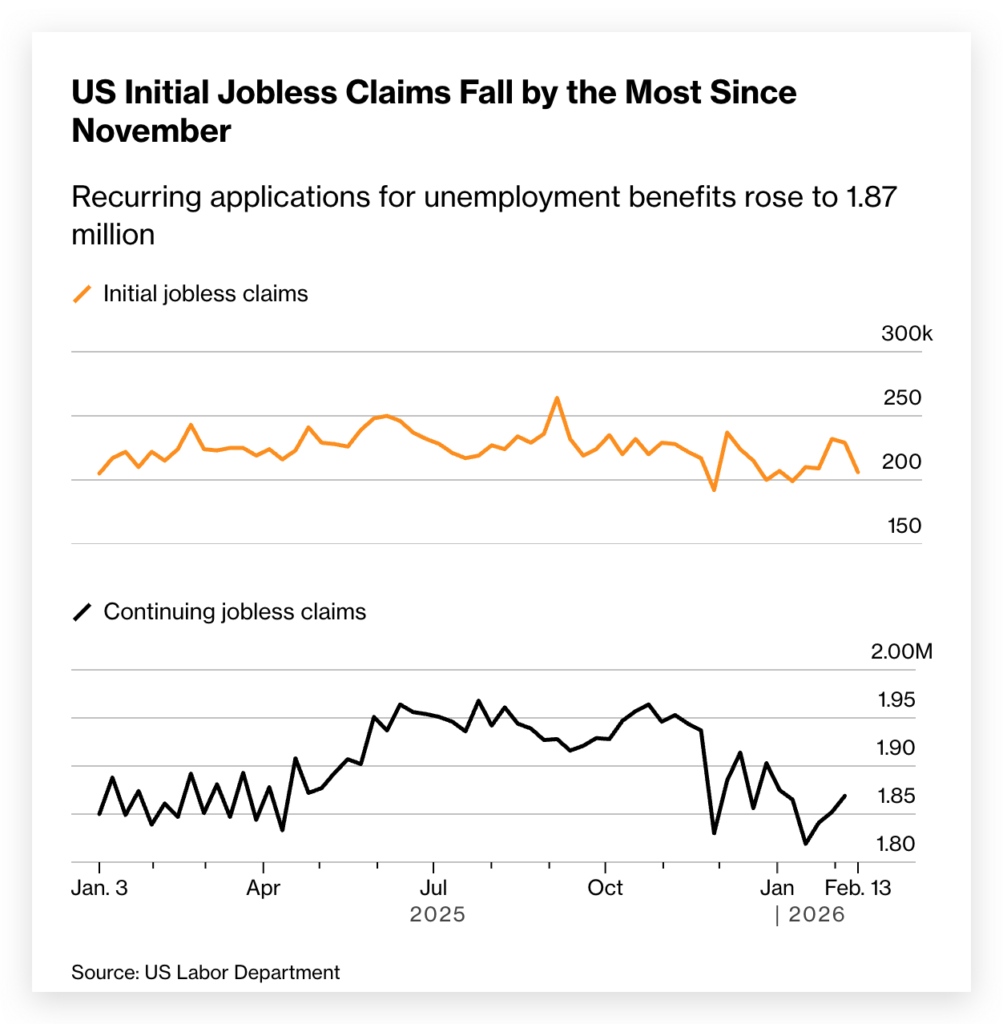

Unemployment

Hiring has cooled, but employers are largely retaining current staff — a dynamic often described as “low hire, low fire.”

Initial jobless claims for the week ending Feb. 14 fell by the most since November, to 206,000, suggesting layoffs remain limited by historical standards. However, continuing claims stand at 1.87 million, indicating many unemployed Americans are struggling to secure new positions.

Inflation

Inflation has fallen significantly from its 2022 peak but has shown limited progress since Trump took office. The Federal Reserve’s preferred measure of underlying price pressures was 3% in December. Consumer prices increased 0.2% in January from the previous month, signaling relatively mild inflation at the start of the year.

Even so, elevated prices remain a political challenge for a president who campaigned on lowering them. Trump has introduced measures aimed at easing housing pressures and capping credit card borrowing costs.

Economic Growth

Trump frequently describes the US as the “hottest country” in the world economically. While growth last year was solid, it slowed toward year-end.

Gross domestic product expanded at a 1.4% annualized pace in the fourth quarter, partly weighed down by a record-long government shutdown. That left full-year growth at 2.2%, down from 2.8% in 2024.

Retail Sales

Retail sales proved resilient through much of 2025 but lost momentum in the second half of the year and unexpectedly stalled in December.

Higher-income households have continued to drive consumption, while lower-income consumers have grown more cautious, possibly reflecting slower wage gains.

Housing

Housing is central to Trump’s affordability agenda. He has proposed limiting home purchases by large institutional investors and urged the Federal Reserve to cut interest rates.

The average 30-year fixed mortgage rate is around 6% as of mid-February, down from roughly 7% at the beginning of Trump’s second term, according to Freddie Mac. Although that’s the lowest level in more than three years, it remains high compared with the decade before 2022, offering only modest relief for buyers and homeowners seeking to refinance.

Home sales and construction remain subdued. Sales of previously owned homes fell in January by the most in nearly four years. While housing starts climbed to a five-month high in December, total starts for the year marked a fourth consecutive annual decline.