US Treasuries just can’t catch a break. After a solid run earlier this month on hopes that inflation was finally cooling enough for the Fed to keep cutting rates, bonds are now staring down their longest losing streak in a month—and it’s all because of oil and the shadow of fresh trouble in the Middle East.

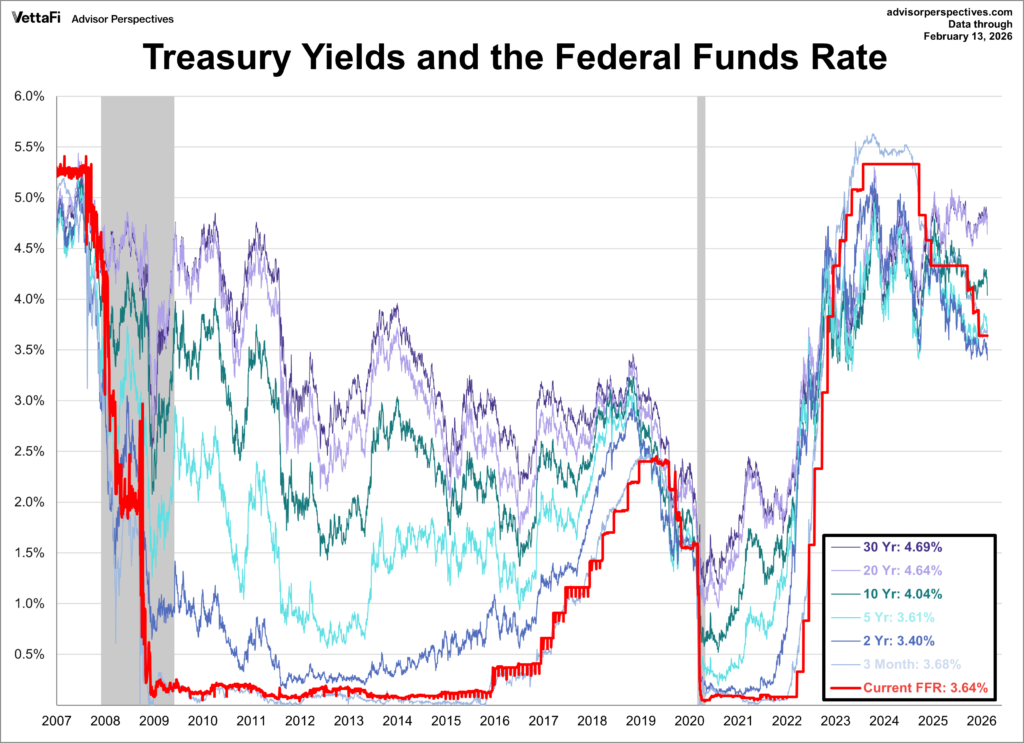

Yields climbed for a third straight day, with the benchmark 10-year note ticking up about a basis point to 4.09 percent in recent trading. The shorter two-year yield, more sensitive to Fed moves, pushed higher too, landing around 3.47-3.48 percent. Traders dumped bonds as oil surged again, with Brent crude climbing toward $71 a barrel and WTI hovering near $66 after a more than 4 percent jump the day before. The spark? Reports that a U.S. strike on Iran could come sooner than anyone thought—maybe even this weekend—amid stalled nuclear talks and military buildup in the region. Iran, the world’s ninth-biggest oil producer, sits right by the Strait of Hormuz; any real disruption there would send energy prices screaming higher and drag inflation right back into the spotlight.

It’s a sharp turnaround from just a couple of weeks ago, when softer January CPI numbers had everyone pricing in more aggressive Fed easing. Now the mood has flipped. Minutes from the Fed’s January meeting, dropped on Wednesday, showed policymakers sounding noticeably more cautious: most are less worried about the job market softening but way more uncomfortable with inflation stubbornly above 2 percent. A few even floated the idea of hiking rates again if things don’t improve fast, and the “upside risks” to their forecasts got highlighted. That hawkish vibe crushed hopes for a March cut and left traders only half-convinced there’ll be even two quarter-point moves later this year.

The dollar jumped to a two-week high on the news, gold spiked back above $5,000 an ounce as the classic safe-haven play, and stock futures wobbled lower in premarket. Everything’s feeding on everything else: higher oil means stickier prices, which means a less dovish Fed, which means higher yields, which means… well, you get it.

Investors are now laser-focused on Friday’s data dump— the January PCE inflation read (the Fed’s favorite gauge) and fourth-quarter GDP numbers. If those come in hotter than expected, this sell-off could accelerate. Meanwhile, the Treasury Department’s getting ready to auction another $9 billion in 30-year TIPS, which should give a pretty clear read on how worried the big money is about long-term inflation staying elevated.

Bottom line: geopolitics just reminded the market that rate-cut dreams can evaporate fast when oil jumps and central bankers start talking tough. For now, the bond bulls are on the sidelines, watching the headlines out of the Gulf and hoping the weekend stays quiet.