Capital Reforms and Nonbank Lending

U.S. regulators are reworking bank capital rules (the Basel III “endgame” proposals) in part to encourage more traditional lending. Fed officials emphasize that “requirements that overly calibrate low-risk activities” can inadvertently constrain credit and push loans into nonbanks[1]. Indeed, since 2008 banks have faced much higher capital charges, and over that period the nonbank private‐credit sector has exploded. Global private-debt fund assets now exceed \$3.5 trillion[2]. The new proposals (over 1,000 pages of rules) would remove duplicate capital buffers and better align risk weights with real risk[1]. For example, regulators plan lighter capital for ordinary mortgages and conservative business loans, on the view that banks should be able to lend more safely under those programs.

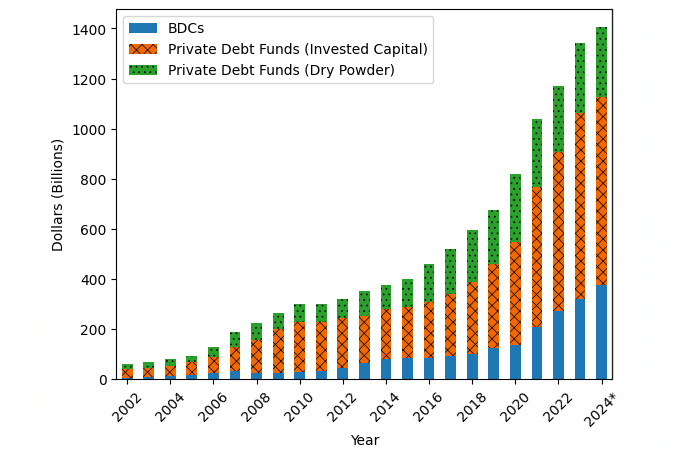

Figure: Global private credit assets (business-development companies and private-debt funds) have surged in recent years[2]. In other words, borrowers have sought more financing outside banks. Banks still dominate core lending, but they increasingly act as lenders-of-last-resort to private credit – for instance by extending warehouse credit lines to BDCs or other loan funds. The capital proposal is meant to make such bank-for-fund lending less onerous. A Fed official explicitly warned that capital rules should not discourage lending to safe borrowers[1].

Securitized Bank Lending

Under the current simplified supervisory formula approach (SSFA), many bank-to-fund loans are treated like senior tranches of securitized pools. For example, a bank might lend to a special-purpose vehicle holding a portfolio of loans (say, senior middle-market loans) but fund only 50% of that portfolio. The bank’s exposure is cushioned by the unfunded portion (overcollateralization). Under SSFA, that senior exposure qualifies for the senior tranche treatment: its risk weight is very low. In fact, the senior piece can get only a 20% risk-weight floor under current rules[3], even though the underlying loans themselves would carry 100%. The 2023 proposal would cut that floor to 15%[4], making such financing even cheaper for banks. (It also imposes a 100% floor on any “re-securitization” or pool of troubled loans[4].) In short, lending to a fund through a securitization-like structure is treated as far less risky than holding the raw loans on the bank’s balance sheet.

Bank vs. Direct Lending Economics

The capital effects are stark. A bank making a loan directly to a borrower (e.g. a corporation) must assign it as a corporate exposure at 100% risk weight[5] (or even 150% if the loan goes bad). That ties up far more capital and erodes return-on-equity. By contrast, a bank extending the same funds to a loan fund (with the collateral structure above) uses much less capital. Researchers quantify this gap: assuming a 15% target capital ratio, a bank’s ROE on a middle-market loan would be only ~15% if held directly, but roughly 24% if made via a private-fund structure[6]. (If the bank targets 12% capital, the gap widens – ~17.5% vs ~46%[6].) In other words, “lending to the lender” can materially boost a bank’s returns[6]. Banks also save on costs by dealing with one borrower (a fund) instead of many companies.

Data on Bank–Nonbank Lending

The effect shows up in lending data. FDIC reports that bank loans to nonbank financial institutions (NBFIs) – including finance companies, lending funds, and BDCs – grew from \$56 billion in 2010 to about \$1.32 trillion by Q3 2025[7]. That is roughly 10% of all bank loans (up from under 1% in 2010)[7]. These NBFI loans now represent over one-third of banks’ commercial lending outside real estate[7]. Large banks dominate this niche: as of Q3 2025, banks with over \$100 billion in assets held ~86% of NBFI loans, and the 10 largest banks held ~71%[8]. This emerging “bank–nonbank nexus” means banks and private funds have become partners in credit provision. (Indeed, a 2025 study finds that private credit generally complements bank lending – expanding overall credit – rather than simply replacing it[9].)

It is not precisely documented how much of banks’ NBFI lending uses the low SSFA weights. Industry analysts estimate U.S. banks have roughly \$900–\$1,000 billion in such on-balance-sheet securitization exposures. Under current SSFA rules, those positions carry only about 20–23% of risk-weighted assets (thanks to the overcollateralization). The new proposal would lower capital charges further on these loans, blurring the line between bank direct lending and bank‐funded lending via intermediaries.

Implications

These Basel III proposals (still subject to comment) tilt incentives noticeably. On one hand, the agencies do propose relief for certain mortgage and retail loans (which would encourage banks to hold more of those). On the other hand, the capital treatment for loans to other lenders becomes even more favorable. In effect, regulators are tacitly approving a partnership model: banks use their funding advantage to back nonbank funds, and in return earn higher ROE on those loans. Fed officials argue this dynamic can be beneficial as long as capital rules reflect risk[1]. Regulators will, however, need to watch the nonbank sector’s stability (liquidity and leverage risks). Overall, the draft rules recognize that banks and private credit funds are not necessarily zero-sum rivals – they can coexist and jointly expand credit availability, provided the risks are appropriately managed[1].

Sources: Official Basel III proposals by the Federal Reserve/OCC/FDIC; Federal Reserve and FDIC data and research (e.g. FDIC Banking Issues in Focus on NBFI lending[7][8]); academic analysis (Chernenko, Ialenti, Scharfstein[6]); and industry research on private credit.[3][4][5][1][9][6][7][8][2]

[1] Michelle W Bowman: Capital rules for the real economy

https://www.mfaalts.org/industry-research/new-study-finds-private-credit-complements-bank-lending

[2] Press Release: Strong growth sees private credit market reach US$3.5 trillion

https://www.mfaalts.org/industry-research/new-study-finds-private-credit-complements-bank-lending

https://www.mfaalts.org/industry-research/new-study-finds-private-credit-complements-bank-lending

[5] eCFR :: 12 CFR Part 3 Subpart D — Risk-Weighted Assets—Standardized Approach

https://www.mfaalts.org/industry-research/new-study-finds-private-credit-complements-bank-lending

[6] bostonfed.org

https://www.mfaalts.org/industry-research/new-study-finds-private-credit-complements-bank-lending

[7] [8] Bank Lending to Nondepository Financial Institutions

https://www.mfaalts.org/industry-research/new-study-finds-private-credit-complements-bank-lending

[9] New study finds private credit complements bank lending – Managed Funds Association

https://www.mfaalts.org/industry-research/new-study-finds-private-credit-complements-bank-lending